Most people think Nvidia got lucky with AI. They made chips that were good for gaming, and it turned out those same chips were good for machine learning.But that's not what happened at all…What actually happened reveals a fundamental misunderstanding of technology markets, and why investors often misread them.

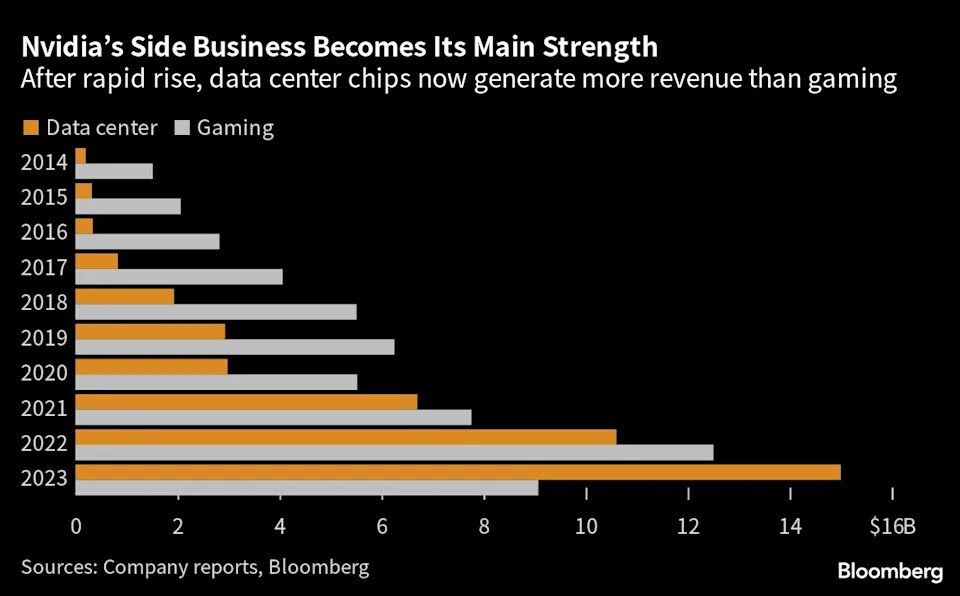

Nvidia’s data center revenue flipped gaming in 2023

Why Markets Misread Platform Plays

Markets consistently undervalue platform investments while they're being made, then overvalue them once they succeed. Platform plays often appear to be terrible business decisions for years before they become obviously valuable.CUDA — Nvidia's software platform that made it possible to harness graphics card compute power for general-purpose usage — is the perfect example of this.When Nvidia was spending heavily on CUDA in the mid-2000s, the market saw it as an expensive distraction from its core graphics business.The investment made no sense. They were giving away free software to sell hardware, in an industry where hardware margins were already under pressure.Markets tend to price such technology investments through the lens of existing applications rather than potential ones. They can see the current build cost but fail to factor in the potential future value.

The Economics of Platform Capture

Technology markets have the somewhat unique capacity to shift from competing products to competing ecosystems.If this shift from product to ecosystem wars occurs, traditional competitive analysis can become almost useless.In a product market, a 10% advantage might translate to a 10% market share gain. In an ecosystem market, a 10% advantage can translate to a 90% market share, due to network effects and switching costs.This is why established companies with superior resources often lose to platform challengers. AMD and Intel both had as much (or more) money and engineering talent as Nvidia during its CUDA development years. But they were competing in the wrong game. They were optimizing for product performance while Nvidia was building ecosystem lock-in.

The Platform Investment Paradox

Platform investments create a paradox for public markets. The companies that make the biggest platform bets often see their stock prices suffer during the investment phase.Product investments have visible, measurable returns that markets can model. Platform investments have uncertain returns that depend on market timing and adoption patterns that are impossible to predict.This is why markets consistently undervalue platform companies during their growth phase. Traditional financial metrics capture the cost of platform investment but miss the value creation occurring in the ecosystem.By the time platform value becomes visible in financial results, the strategic opportunity has usually already passed. The companies that capture platform markets are typically those that invest before the value is measurable, not after it becomes obvious.

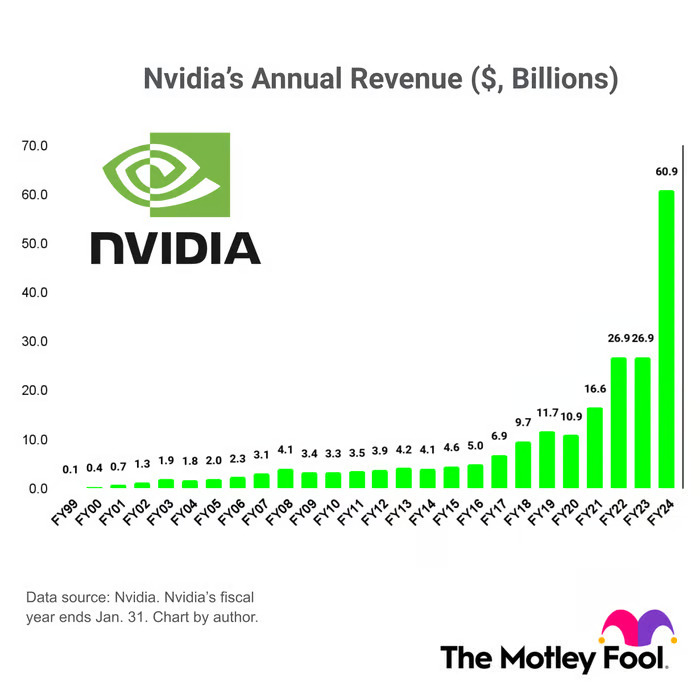

Nvidia’s 25-year Annual revenue growth - image by Motley Fool

Ecosystem Network Effect

Every developer who learns CUDA makes the Nvidia ecosystem more valuable. Every model trained on Nvidia infrastructure increases switching costs for the entire AI market.Gaining a competitive advantage in platform markets is more about ecosystem momentum than building superior products. The platform that attracts the most developers and creates the most applications becomes increasingly difficult to displace.Markets often misinterpret this momentum as a temporary competitive advantage rather than recognizing it as a structural shift in the market. They keep expecting "competition" to erode platform dominance, not realizing that successful platforms tend to make competition irrelevant.

What This Means for Market Analysis

The Nvidia pattern suggests that technology market analysis needs to focus more on ecosystem dynamics and less on product comparisons. The companies that will dominate the next wave of technology markets are likely building platforms today for applications that don't yet exist at scale.This requires looking beyond current revenue and margins to understand what infrastructure is being built for the future. The most important question isn't whether a company has the best current product, but whether they're creating the ecosystem that future applications will be built on.Of course, such companies are unlikely to achieve the heights of Nvidia, but the ones that find success will likely follow the same pattern — years of patient platform building followed by explosive ecosystem capture when the market inflection point arrives.Trade Nvidia and thousands of other Share CFDs on GO Markets — starting from just US$0.02 per share with no monthly data fee.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.